English

Union Budget 2026: Date, Structure, Process, Highlights & Download PDF

Every year, the presentation of the Union Budget marks one of the most consequential moments in India’s governance calendar. It is not merely a statement of accounts, but a comprehensive expression of the Government’s economic priorities, fiscal strategy, and policy direction for the coming year. Through the Budget, the State decides how resources will be raised, where they will be spent, and what kind of economic path the country will pursue.

The Union Finance Minister presented the Union Budget 2026 in Parliament on 1st February 2026. As with previous years, it follows the release of the Economic Survey and draws heavily from the assessment and themes outlined in it.

The official Union Budget 2026–27 Speech and key features PDF can be downloaded from the India Budget Portal or the link provided below.

Union Budget 2026-27 Speech – Download PDF (Official)

Key Features of Union Budget 2026-27 – Download PDF (Official)

What is the Union Budget?

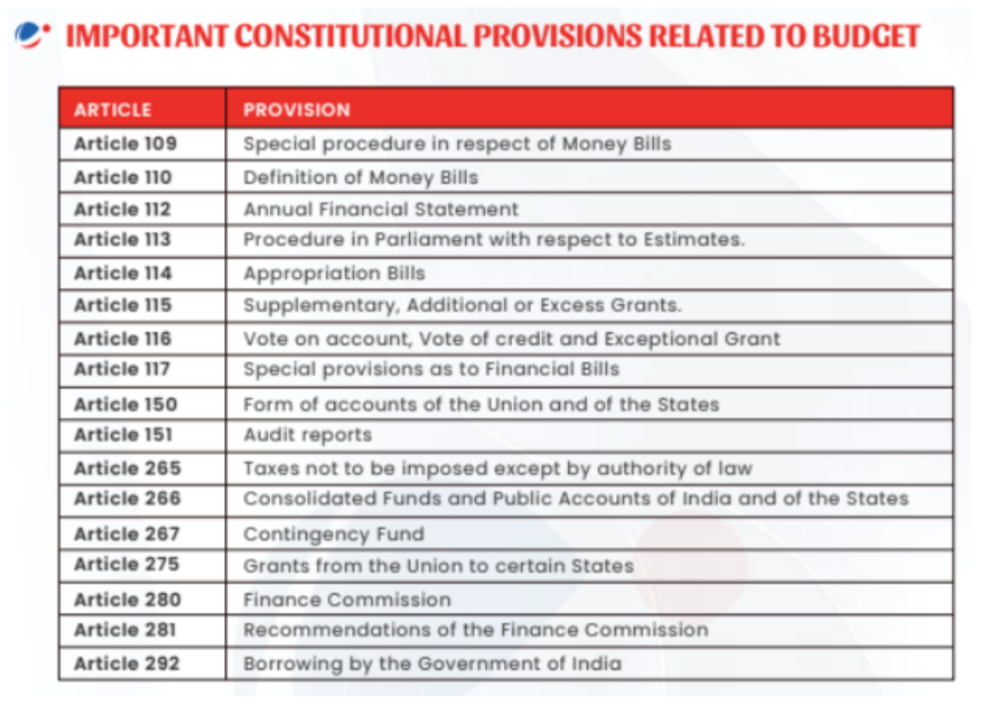

In constitutional terms, the Budget is referred to as the Annual Financial Statement under Article 112 of the Constitution of India. It is a statement of the estimated receipts and expenditure of the Government of India for a financial year.

Interestingly, the word “Budget” itself does not appear in the Constitution, but the document performs one of the most critical constitutional functions: seeking Parliament’s approval for taxation and expenditure.

In practical terms, the Union Budget reflects:

- The Government’s development priorities

- Its assessment of economic challenges and opportunities

- Its approach towards growth, welfare, infrastructure, and fiscal discipline

- Its vision for resource mobilisation and allocation

The Union Budget is prepared by the Department of Economic Affairs in the Ministry of Finance.

A Brief History of Budget in India

India’s budgetary tradition dates back to the colonial period. The first budget in India was presented on 7th April 1860 by James Wilson, who was the first Finance Member of the Viceroy’s Council.

After Independence, the first budget of independent India was presented on 26th November 1947 by R. K. Shanmukham Chetty.

Over time, the Budget has evolved from a narrow fiscal document into a comprehensive policy instrument shaping India’s economic and social transformation.

The Budget Process: From Presentation to Law

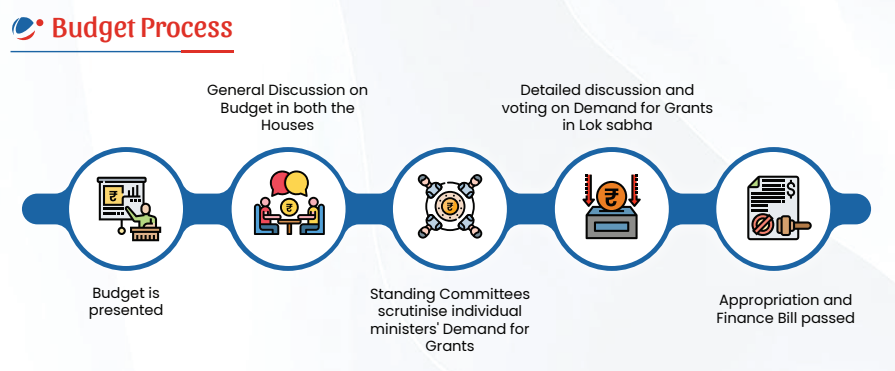

The journey of the Budget through Parliament is a structured constitutional and parliamentary process.

It begins with the presentation of the Budget in both Houses of Parliament. This is followed by a general discussion, where members debate the broad themes and priorities of the Budget.

After this, the Department-related Standing Committees of Parliament examine the Demands for Grants of various ministries in detail. Their reports form the basis for further discussion in the Lok Sabha.

Subsequently, the Demands for Grants are discussed and voted upon in the Lok Sabha. Once this stage is completed, the Appropriation Bill and the Finance Bill are passed, which gives the Government legal authority to withdraw money from the Consolidated Fund of India and to implement taxation proposals.

Thus, the Budget becomes both a policy statement and a legal instrument.

How the Union Budget is Structured ?

At a broad level, the Budget is classified into:

Revenue Budget and Capital Budget

The Revenue Budget deals with the Government’s routine receipts and expenditure. It includes tax revenue, non-tax revenue, and expenditure on administration, subsidies, interest payments, and other day-to-day functions of the State.

The Capital Budget, on the other hand, deals with long-term financial flows. It includes capital receipts such as borrowings and disinvestment, and capital expenditure such as infrastructure creation, asset building, and long-term investments.

Two Conceptual Parts of the Budget

From a policy perspective, the Budget can also be seen in two parts:

- The Macroeconomic and policy part, which reflects government priorities, sectoral focus, and resource allocation strategy.

- The Finance Bill part, which deals with taxation proposals, changes in tax laws, and fiscal provisions.

Together, these two give both the direction and the legal framework of the Budget.

Major Budget Documents

Apart from the Finance Minister’s Budget Speech, the Union Budget consists of several important documents

Together, these documents provide a complete picture of the Government’s fiscal strategy and policy intent.

Download VisionIAS previous Year’s summary of Union Budget 2025-26

Union Budget 2026: Highlights

(To be updated)

How UPSC Aspirants Should Read the Budget 2026

For UPSC aspirants, the Budget 2026 is not important because of its size, but because of its policy orientation and analytical depth. It is crucial for:

- GS Paper III (Indian Economy, Government Budgeting, Growth and Development)

- Essay (themes like welfare, growth, state capacity, reforms, inclusive development)

- Interview (policy awareness and economic understanding)

The focus should always be on:

- Priorities and policy direction, not just numbers

- Continuity and change in government strategy

- Linkages with Economic Survey and previous years’ policies

- Implications for governance and development

VisionIAS Economy Sprint – Economic Survey & Union Budget for UPSC 2026

The Economic Survey and the Union Budget together form the most important current affairs cycle of the year for the Indian economy. To help aspirants:

- Build strong conceptual clarity in economics

- Understand Survey and Budget in an integrated manner

- Connect static concepts with live policy decisions

- Practice through focused and exam-oriented questions

VisionIAS offers a 2-week focused Economy Sprint program covering:

- Core economics concepts

- Chapter-wise Economic Survey analysis

- Dedicated Budget interpretation session

- Integrated quizzes on Digital Current Affairs (DCA) platform

- Sandhan Current Affairs with 5000+ UPSC-level MCQs drawn from monthly current affairs and PT 365 of the current and previous years

- One-to-one mentoring support and guidance

In a UPSC preparation journey where time and clarity matter, such focused modules help convert information into understanding and understanding into marks.

Know more and register, VisionIAS Economy Sprint – Economic Survey & Union Budget for UPSC 2026

Conclusion

The Union Budget 2026 will not only decide how resources are allocated for the coming year, but will also reveal how the Government views India’s economic challenges and opportunities in the medium term. For serious UPSC aspirants, it is not a document to be skimmed, but a framework to be understood.

FAQs on Union Budget 2026–27

Q1. What is the Union Budget 2026–27?

The Union Budget 2026 is the annual financial statement of the Government of India that outlines estimated revenues and expenditures for the financial year 2026–27, along with fiscal policy priorities and economic measures.

Q2. Who presents the Union Budget 2026?

The Union Budget 2026–27 is presented in Parliament y the Union Finance Minister of India.

Q3. When is the Union Budget 2026–27 presented?

The Union Budget 2026 will be presented on 1 February 2026 during the Budget Session of Parliament.

Q4. Under which Article of the Constitution is the Union Budget presented?

The Union Budget is presented under Article 112 of the Constitution of India, which mandates the presentation of the Annual Financial Statement.

Q5. What are Demands for Grants?

Demands for Grants are detailed statements showing the estimated expenditure of each ministry and department, which require approval by the Lok Sabha before funds can be withdrawn from the Consolidated Fund of India.

Q6. What is expected in the Union Budget 2026?

The Union Budget 2026 is expected to focus on economic growth, infrastructure development, employment generation, fiscal consolidation, and social sector priorities, in line with prevailing economic conditions.