Current Affairs

Pradhan Mantri Mudra Yojana Marks 11 Years of Funding the Unfunded

The Pradhan Mantri MUDRA Yojana (PMMY) launched by the Prime Minister of India on April 8, 2015, marks 11 years of success in strengthening India’s grassroots entrepreneurs.

Pradhan Mantri Mudra Yojana (PMMY) completed 11 years on April 8, 2026, a milestone that marks over a decade of collateral-free credit access for India’s micro and small entrepreneurs.

Since its launch by the Prime Minister of India in 2015, the scheme has disbursed over ₹40.07 lakh crore through 57.79 crore loans, making it one of the most expansive financial inclusion initiatives in the world.

What is PM Mudra Yojana?

Pradhan Mantri Mudra Yojana (PMMY) is a flagship Central Sector Scheme launched by the Government of India in 2015 with the objective of providing affordable, accessible, and collateral-free credit to the vast segment of non-corporate, non-farm micro and small enterprises. These enterprises often face difficulties in accessing formal institutional finance due to lack of collateral, credit history, or documentation.

The core philosophy of the scheme is encapsulated in its mission statement, “Fund the Unfunded”, which aims to bring such underserved entrepreneurs into the formal financial system, promote financial inclusion, and generate employment at the grassroots level. By facilitating credit access, the scheme also contributes to fostering entrepreneurship, especially among women, SC/ST communities, and other marginalized sections.

The implementation of PMMY is carried out through a wide network of Member Lending Institutions (MLIs), which include Public Sector Banks, Private Sector Banks, Regional Rural Banks (RRBs), Non-Banking Financial Companies (NBFCs), Microfinance Institutions (MFIs), and Small Finance Banks. These institutions are responsible for directly extending loans to eligible borrowers.

At the apex level, MUDRA (Micro Units Development & Refinance Agency Ltd.) plays a crucial role as a refinancing agency. It provides refinance support to these lending institutions, develops guidelines, and ensures the smooth functioning of the scheme. Importantly, MUDRA itself does not lend directly to beneficiaries but acts as a facilitator to strengthen the credit delivery ecosystem.

Loan Categories Under PMMY

PM Mudra Yojana offers loans under four tiers based on the borrower’s stage of growth:

- Shishu: Loans up to ₹50,000 (for early-stage micro enterprises)

- Kishor: Loans from ₹50,000 to ₹5 lakh

- Tarun: Loans from ₹5 lakh to ₹10 lakh

- TarunPlus: Loans from ₹10 lakh to ₹20 lakh (newly introduced)

These loans cover both term financing and working capital needs across manufacturing, trading, service, and agri-allied sectors such as dairy, poultry, and beekeeping.

Key Achievements: 11 Years of Impact

Massive Credit Outreach

Since inception, Pradhan Mantri Mudra Yojana has sanctioned over 57.79 crore loans worth ₹40.07 lakh crore. The year-wise data reflects consistent and growing demand:

| Financial Year | Loans Sanctioned (Crore) | Amount Sanctioned (₹ Lakh Crore) |

| 2015-16 | 3.49 | 1.37 |

| 2019-20 | 6.23 | 3.37 |

| 2023-24 | 6.67 | 5.41 |

| 2024-25 | 5.47 | 5.53 |

| 2025-26 (till Mar 2026) | 4.49 | 5.65 |

Women Entrepreneurship at the Forefront

One of the most significant achievements of PM Mudra Yojana is its reach among women. Around two-thirds of all PMMY loans have gone to women borrowers. In FY 2022 alone, women held approximately 71.4% of total accounts. Under the Shishu category, ₹9.02 lakh crore was disbursed to women reflecting the scheme’s role in democratising entrepreneurship and empowering women.

Inclusion of Marginalised Communities

The scheme has ensured that SC, ST, and OBC communities are not left behind. Around 49% of total loan beneficiaries belong to these groups. The Shishu category’s high share among SC, ST, and OBC borrowers reflects the scheme’s strong grassroots penetration.

New Entrepreneurs and First-Time Borrowers

Approximately one-fifth of all loans were extended to first-time entrepreneurs, amounting to ₹12 lakh crore across 12.15 crore accounts. This reflects the scheme’s ability to create new economic participants rather than just catering to existing businesses.

Bringing Financial Discipline at Grassroots level

Non-Performing Assets (NPAs) have reduced to 2.3%, which is one of the lowest in the world. Financial discipline is no longer limited to big institutions; it is now firmly strengthening at the grassroots. With relatively low NPAs and reduced risk for banks, Mudra has successfully built trust in the system.

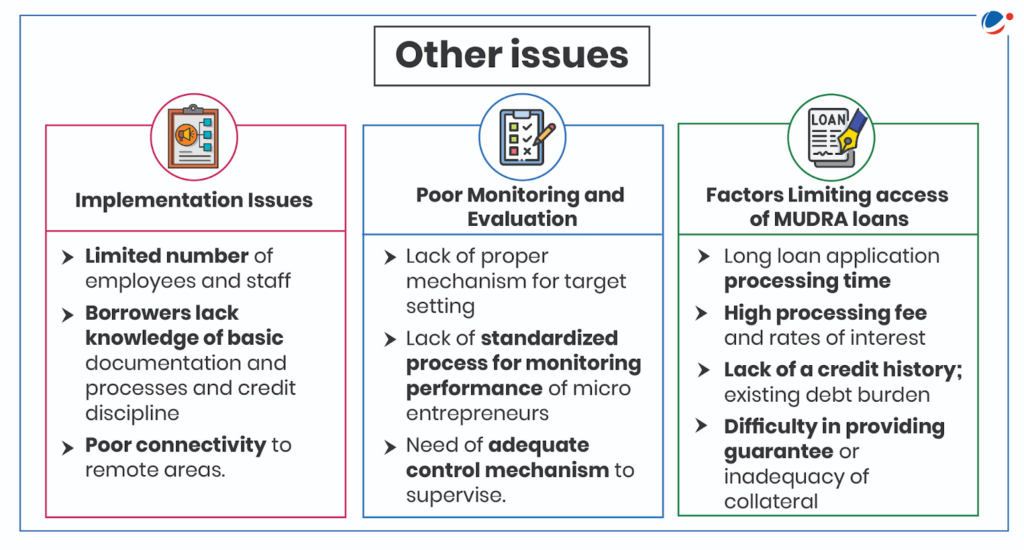

Challenges and Areas for Improvement

Despite its successes, PM Mudra Yojana faces several persistent challenges that need attention.

Institutional and Design Gaps

Several structural issues affect smooth implementation:

- The 15% cap on payouts under Credit Guarantee Fund for Micro Units (CGFMU) reduces banks’ willingness to lend to riskier micro borrowers.

- The claim settlement process under CGFMU is complicated, with slow uploads and technical errors.

- High guarantee fees and refinancing rates increase costs for lenders.

- The lack of a centralized database makes monitoring and data-based decision-making difficult.

Access and Awareness Constraints

Many potential beneficiaries, especially in rural areas, face challenges due to limited awareness, complex documentation requirements, and lack of guidance in accessing loans.

Gender and Socioeconomic Barriers

Women entrepreneurs often face gender bias within financial institutions, along with social constraints such as limited mobility, lower financial literacy, which restrict their participation.

Way Forward

To ensure Pradhan Mantri Mudra Yojana continues to deliver on its mandate, several reforms are recommended:

- Awareness and Outreach: Expanding both traditional advertising (TV, radio, regional-language print) and digital marketing (social media etc.) to reach underserved pockets, particularly in the Northeast and aspirational districts.

- Digitisation of Lending: A unified digital portal for real-time beneficiary data upload can improve transparency and reduce administrative delays.

- Query Redressal Mechanisms: Dedicated chatbots and feedback portals for MLIs and borrowers can ensure faster resolution of operational and technical issues.

- Incentive Structures: Introducing a recognition mechanism for well-performing MLIs can encourage higher-quality lending and better recovery practices.

- Group Lending Models: Best practices like those of Bandhan Bank and IndusInd Bank, which use group-based lending to build accountability, have shown success in reducing NPAs and can be scaled across more lenders.

Conclusion

Completing 11 years of PM Mudra Yojana is a milestone worth reflecting on both for what has been achieved and what remains unfinished. The scheme has fundamentally altered India’s credit landscape for micro and small entrepreneurs, brought crores of first-generation borrowers into the formal financial system, and made women the central beneficiaries of institutional credit.

Yet, institutional bottlenecks and challenges to access signal that Pradhan Mantri Mudra Yojana must continue to evolve. As India marches toward Viksit Bharat 2047, the scheme’s success in “Funding the Unfunded” will remain a cornerstone of inclusive economic growth.

Master Digital Age Governance & Technology Trends with VisionIAS Comprehensive Current Affairs →

Pradhan Mantri Mudra Yojana FAQs

1. What is the Pradhan Mantri Mudra Yojana (PMMY)?

Ans. It is a collateral-free credit scheme for micro and small enterprises.

2. When was the Pradhan Mantri Mudra Yojana launched?

Ans. It was launched on 8 April 2015.

3. What is the primary objective of PM Mudra Yojana?

Ans. Its objective is to fund the unfunded and promote financial inclusion.

4. Who are the eligible beneficiaries under PMMY?

Ans. Non-corporate, non-farm micro and small enterprises are eligible.

5. What are the different loan categories under PM Mudra Yojana?

Ans. The categories are Shishu, Kishor, Tarun, and TarunPlus.